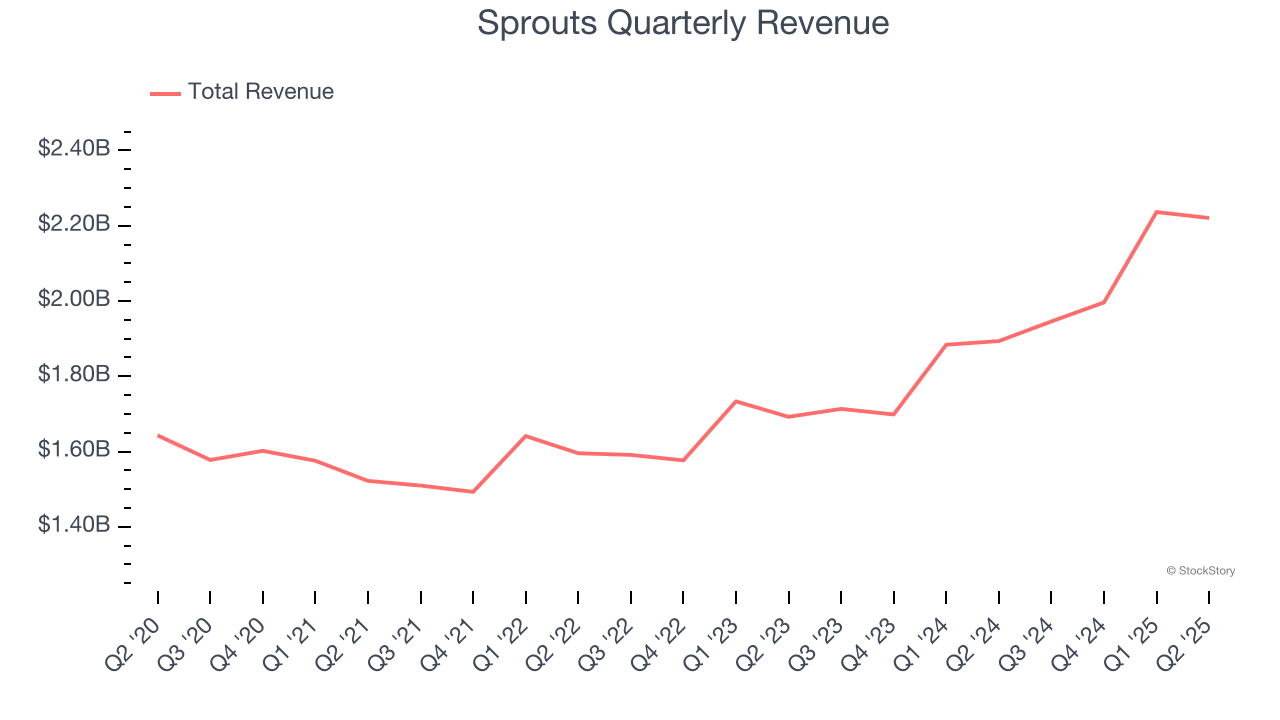

Grocery store chain Sprouts Farmers Market (NASDAQ:SFM) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 17.3% year on year to $2.22 billion. Its GAAP profit of $1.35 per share was 9.4% above analysts’ consensus estimates.

Is now the time to buy Sprouts? Find out by accessing our full research report, it’s free.

Sprouts (SFM) Q2 CY2025 Highlights:

- Revenue: $2.22 billion vs analyst estimates of $2.17 billion (17.3% year-on-year growth, 2.3% beat)

- EPS (GAAP): $1.35 vs analyst estimates of $1.23 (9.4% beat)

- Adjusted EBITDA: $217.8 million vs analyst estimates of $200.5 million (9.8% margin, 8.6% beat)

- EPS (GAAP) guidance for the full year is $5.26 at the midpoint, beating analyst estimates by 3.3%

- Operating Margin: 8.1%, up from 6.7% in the same quarter last year

- Free Cash Flow Margin: 2.3%, similar to the same quarter last year

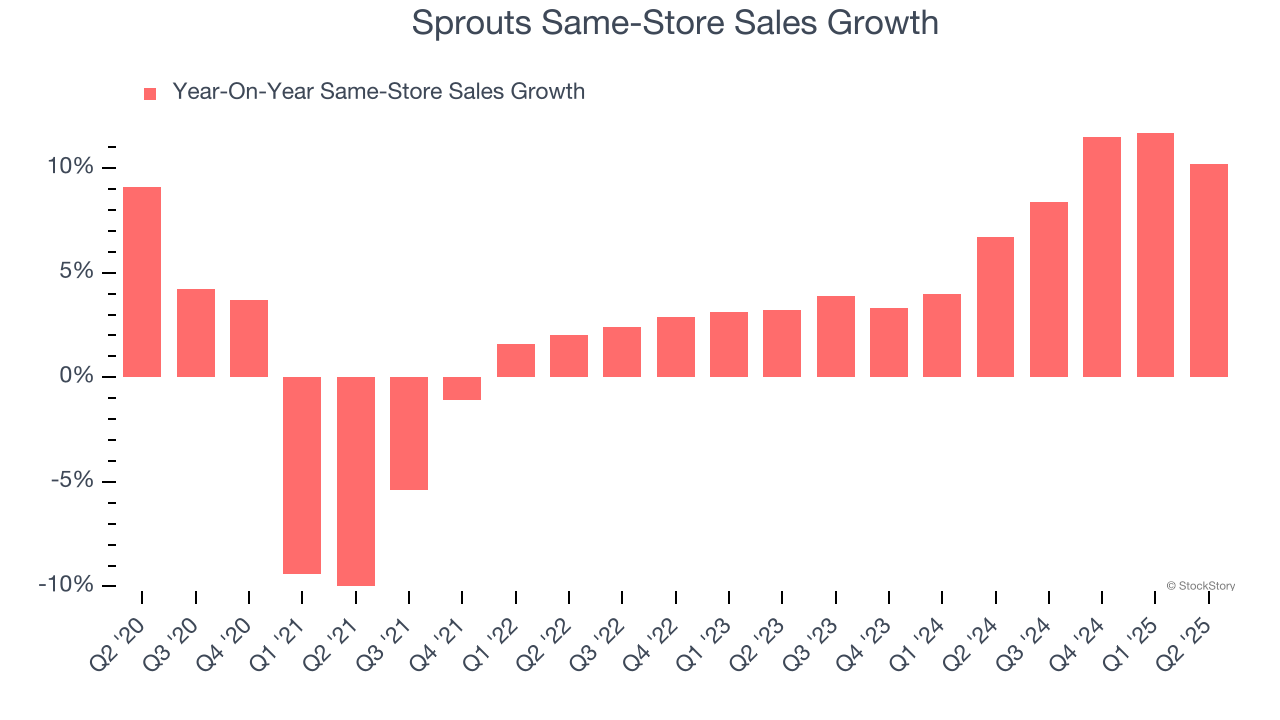

- Same-Store Sales rose 10.2% year on year (6.7% in the same quarter last year)

- Market Capitalization: $15.36 billion

"We are pleased with our excellent results for the second quarter," said Jack Sinclair, chief executive officer of Sprouts Farmers Market.

Company Overview

Playing on the secular trend of healthier living, Sprouts Farmers Market (NASDAQ:SFM) is a grocery store chain emphasizing natural and organic products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $8.40 billion in revenue over the past 12 months, Sprouts is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Sprouts grew its sales at a mediocre 7.5% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts), but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Sprouts reported year-on-year revenue growth of 17.3%, and its $2.22 billion of revenue exceeded Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 10.2% over the next 12 months, an acceleration versus the last six years. This projection is eye-popping and indicates its newer products will spur better top-line performance.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Store Performance

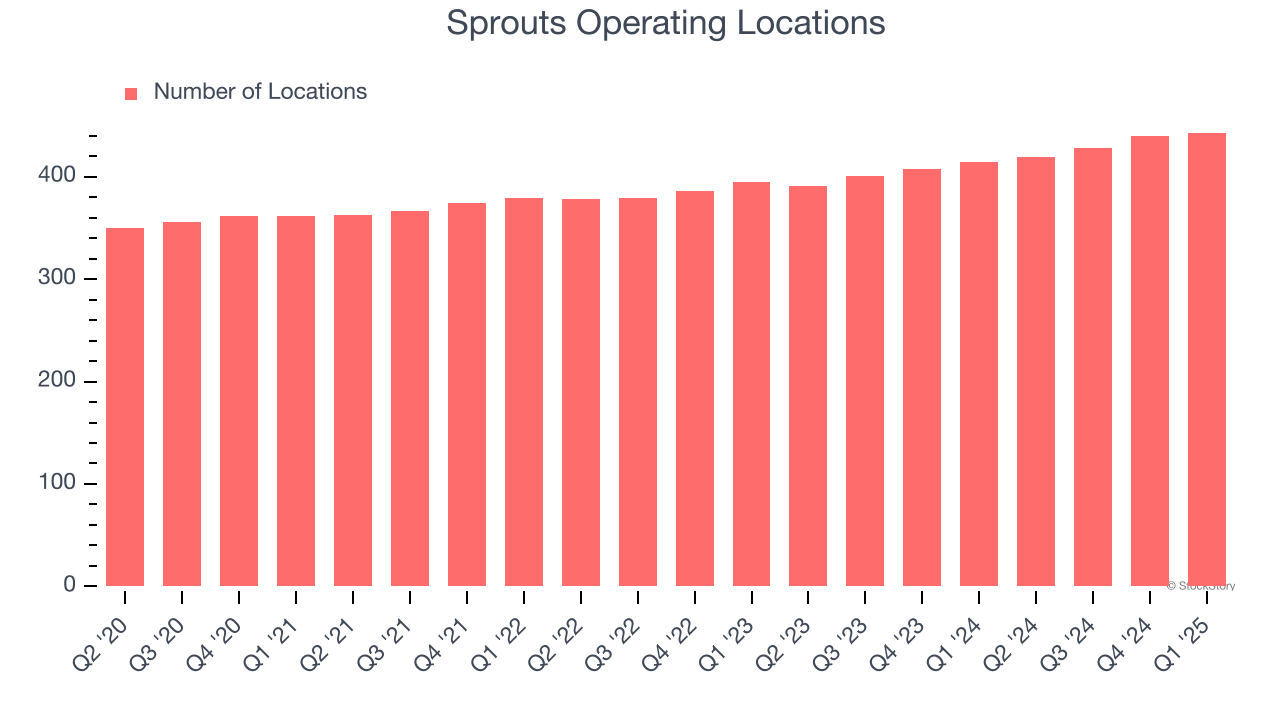

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Over the last two years, Sprouts opened new stores at a rapid clip by averaging 6.4% annual growth, among the fastest in the consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Sprouts reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Sprouts has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 7.5%. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Sprouts multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Sprouts’s same-store sales rose 10.2% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Sprouts’s Q2 Results

We were impressed by how significantly Sprouts blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.5% to $162.01 immediately following the results.

Sprouts put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.